Humans are not rational. See (Dostoevsky 1864), the parable of the destroying free will. In this note we will describe some behavioural economics ideas that could be interesting in this side. We will see dopamine response will be very important in this context, and see how we can interpret it as an utility.

Economical Games

The rules of the Ultimatum game

The proposer makes an offer as to how this money should be split between the two. The second player (the risponder) can either accept or reject this offer. If it is accepted, the money is split as proposed, but if the risponder rejects the offer, then neither player receives anything.

From a purely rational stand, you should always accept. But humans tend to reject offers that are unfair, even if it means they will get nothing. This is a clear example of how humans are not purely rational. Perhaps you can interpret this in a future relationship manner, if you have an unfair partner, it is not ok for you to work with him/her, so makes sense to reject the relationship. There is some reward system which is not tied to just money.

Humans tend to reject much more compared to computer counterparts who just have this context.

This is explained by the presence of other factor within this game: This introduces:

- Social preferences (altruism, reciprocity, inequality aversion)

- Emotional factors (anger, pride)

- Evolutionary logic (punishing unfairness may deter exploitation in future interactions)

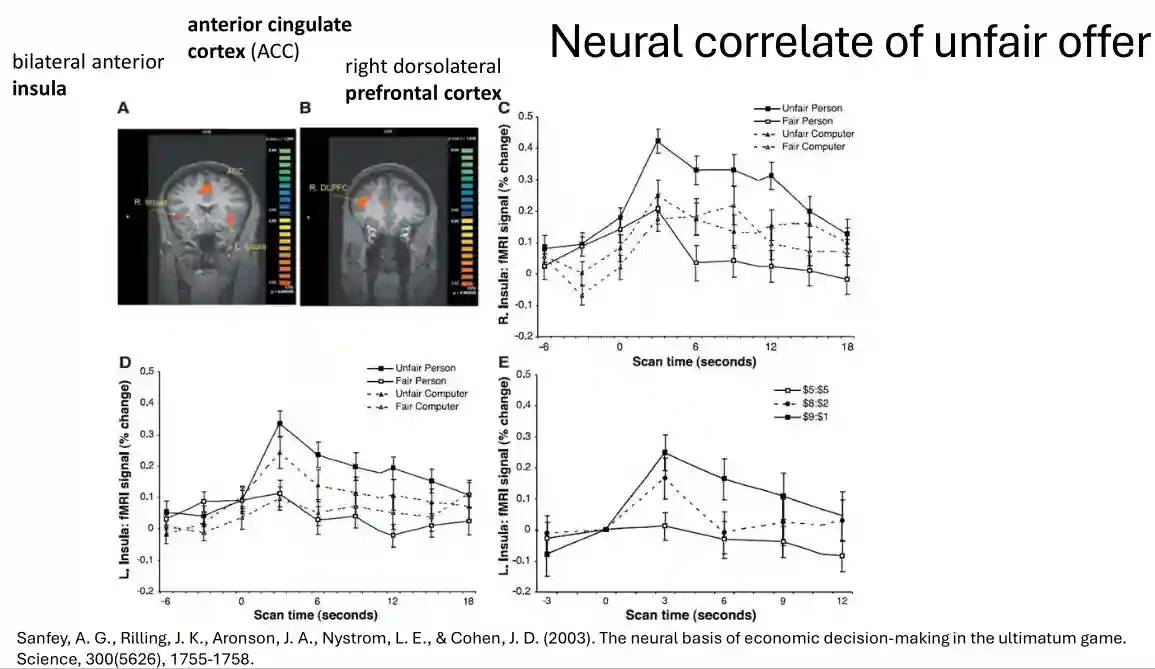

Analysis of Activations in the brain

ACC, conflict detection, attention, performance monitoring, impulse working memory. The insula is emotions, self-awareness, social, and negative emotions, it activates very strongly for unfair parts, probably insula detects the disgust or anger part, the unfair offer. We see the human value lives not just for maximizing money. The emotional part plays a role.

These are some regions associated to the activations while working with the Ultimatum game.

- The anterior insula, tied to emotional responses like disgust or anger, was more active, especially when unfair offers were rejected PubMedEurope PMC.

- The dorsolateral prefrontal cortex (DLPFC), a region associated with cognitive control and deliberative reasoning, was also engaged PubMedTaylor & Francis.

St.Petersburg Paradox

The relative value is very important, not just absolute value.

$$ E = \sum_{k=1}^{\infty} \frac{1}{2^{k}} 2^{k} = \sum_{k=1}^{\infty} 1 = \infty $$A fair coin is tossed at each stage. The initial stake begins at 2 dollars and is doubled every time tails appears. The first time heads appears, the game ends and the player wins whatever is the current stake. Thus, the player wins 2 dollars if heads appears on the first toss, 4 dollars if tails appears on the first toss and heads on the second, 8 dollars if tails appears on the first two tosses and heads on the third, and so on.

Yet, most people would not be willing to pay more than 10 dollars to play this game. This is an example of how humans are not purely rational, or the rationality part is not capturing human reasoning well. I would believe the second.

Expected Utility Theory

We introduce this theory to explain how the above paradox can be resolved. Other resolutions are:

- Risk aversion: Real people discount rare massive wins because the probabilities are so tiny.

Main idea of the theory

The value of an item is not based on the price, but rather on the utility it yields (100$ is more to a poor person than to a rich person).

This idea makes sense. It is also reflected in the bible, while one poor person donates a lot of what it has, its nice.

There is also an example in the scriptures that like the widow that gives a small amount, but it is a lot for her. This is an example of how humans are not purely rational, or the rationality part is not capturing human reasoning well.

$$ U(x) = \sum_{i=1}^{n} p_i u(x_i) $$Where $u(x)$ is the utility function, and $p_i$ is the probability of each outcome.

$$ \sum_{i=1}^{n} p_i u(x_i) - c = 0 $$Marginal Utility

See Budget and Preferences for more info on the economical side.

Individuals make economic decisions by weighing the benefits of consuming an additional unit of a good or service against the cost of acquiring it. In other words, value is determined by the additional utility of satisfaction provided by each extra unit consumed. (source Wikipedia)

This is a general economical concept assumed in economy. Meaning the slope of the satisfaction with respect to the quantity, becomes more planar as the quantity is higher. We have to take specific consideration of this hypothesis, because

$$ \frac{dU}{dg} = \frac{dU}{dx} \cdot \frac{dx}{dg} $$When the second derivative is negative, then it is a diminishing marginal utility.

Modeling Money Utility

$$ U(\omega) = \ln (\omega) $$The expected utility is dependent on the initial capital of the person. We are interested in incremental utility, which means at what stage its good for you to continue investing more, that is the theoretical point where you have good things.

$$ E[U] = \sum_{i} P(z_{i}) U(\omega(z_{i})) $$Where $z_{i}$ is an event, and $\omega(z_{I})$ is its associated value and $P(z_{i})$ is the probability of that event happening. For individual gambles, the value is reshaped to $\omega(z_{i}) - c$.

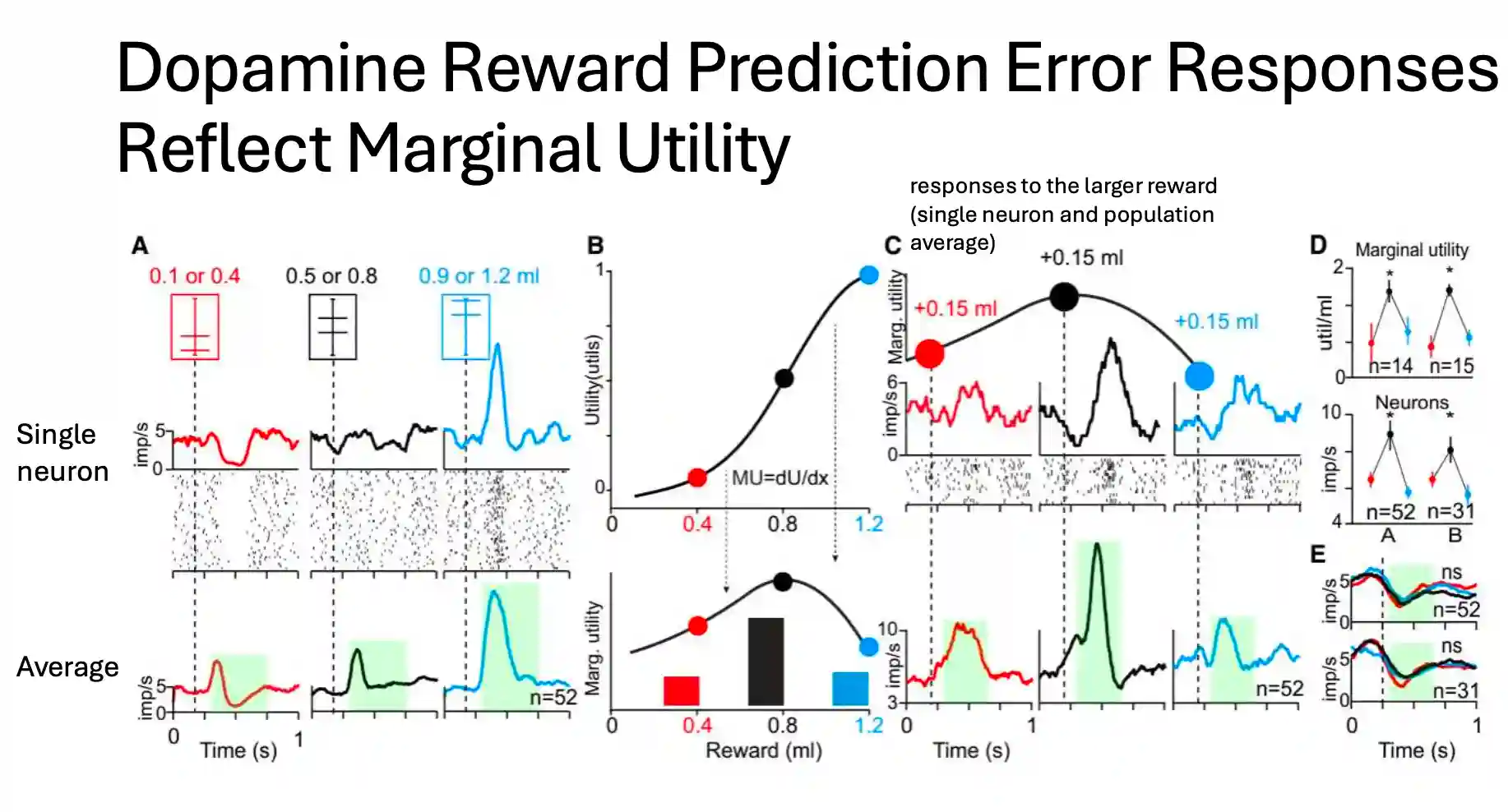

Monkey’s Utility function in risk-based settings

Here they study choices for monkeys in risky and safe settings, the authors wanted to discover how much award would be enough for the monkey to convert and commit to certain choices.

Certainty equivalent: the amount of safe reward that led to choice indifference

The main takeaway from this paper is that dopamine responses are correlated to the marginal utility function for the gambling games the authors have devised.

Dopamine prediction error responses code marginal utility, a fundamental economic variable that reflects risk preferences

On the high end (safe reward high) they were risk-averse, while on the low end they were usually risk-seeking, this means that marginal utility theory is able to explain the behaviour of the animal in this settings. Dopamine reward prediction error responses reflect marginal utility.

Neurons encode utility and not absolute reward. But other parts are not well explained by marginal utility.

They argue the utility of the function changes, that is when dopamine is important. This correlates with the prediction error (remember dopaminergic prediction in the brain).

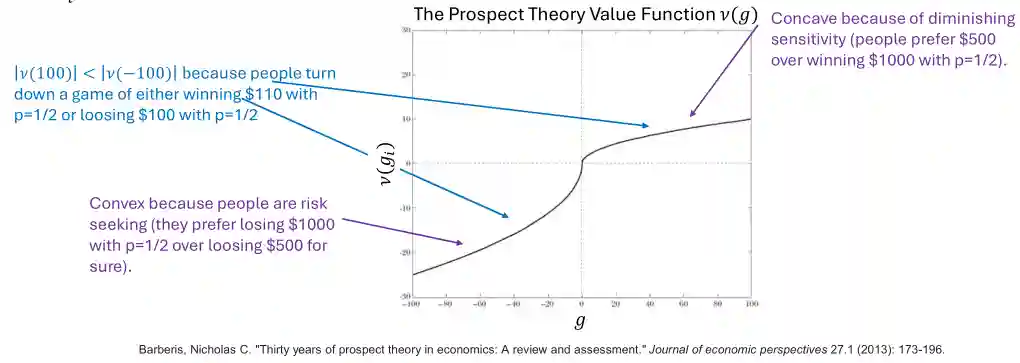

Cumulative Prospect Theory

Framing problem

This is something similar with the copy machine study: (Langer et al. 1978). This was discovered by Kahneman and also discussed in (Kahneman 2011), basically even if you express the same thing, the framing is dramatically different.

•Program A: “200 people will be saved” •Program B: “there is a 1/3 probability that 600 people will be saved, and a 2/3 probability that no people will be saved” -> 72 percent preferred program A •Program C: “400 people will die” •Program D: “there is a 1/3 probability that nobody will die, and a 2/3 probability that 600 people will die” -> 78% preferred program D

The Cumulative Prospect theory

People evaluate gains and losses relative to a reference point, not absolute outcomes.

$$ V(x) = \sum_{i=1}^{n} p_i v(x_i) $$Where $x_i$ is the outcome of the gamble, $p_i$ is the probability of each outcome, and $v(x)$ is the value function.

People are loss averse, this means that usually the value function is concave for gains and convex for losses, which means that people are risk averse for gains and risk seeking for losses. Concave means they are are risk averse, while other one is risk-seeking.

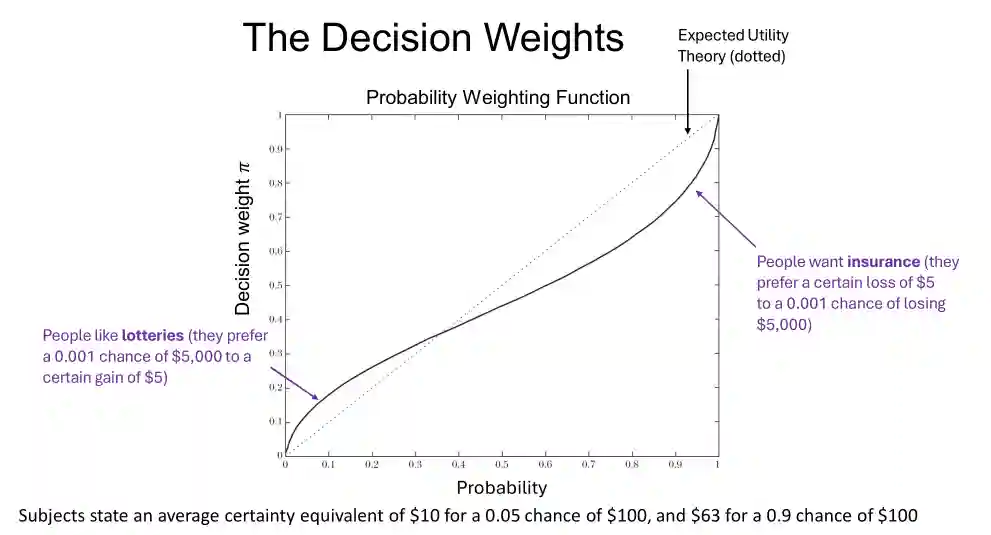

Decision weights

Risk seeking and risk averse. Attempts to solve the linearity of expected utility theory.

Usually you would defines this with respect to a reference point, but this is often not so clear.

References

[1] Kahneman “Thinking, Fast and Slow” Farrar, Straus and Giroux 2011

[2] Dostoevsky “Notes from Underground” Wm. B. Eerdmans Publishing 1864

[3] Langer et al. “The Mindlessness of Ostensibly Thoughtful Action: The Role of "Placebic" Information in Interpersonal Interaction” Journal of Personality and Social Psychology Vol. 36(6), pp. 635--642 1978